Reshaping the Vanadium Industry: From Steelmaking By-Product to a Core Energy Storage Material

Classification:Industrial News

- Author:ZH Energy

- Release time:May-28-2026

【 Summary 】High-temperature stability of vanadium electrolyte is now the most urgent research focus. Improving it can enhance utilization, lower costs, increase energy efficiency, and reduce operating consumption—key factors for broader market adoption of vanadium flow batteries.

From a Steelmaking Additive to a Key Player in Energy Storage

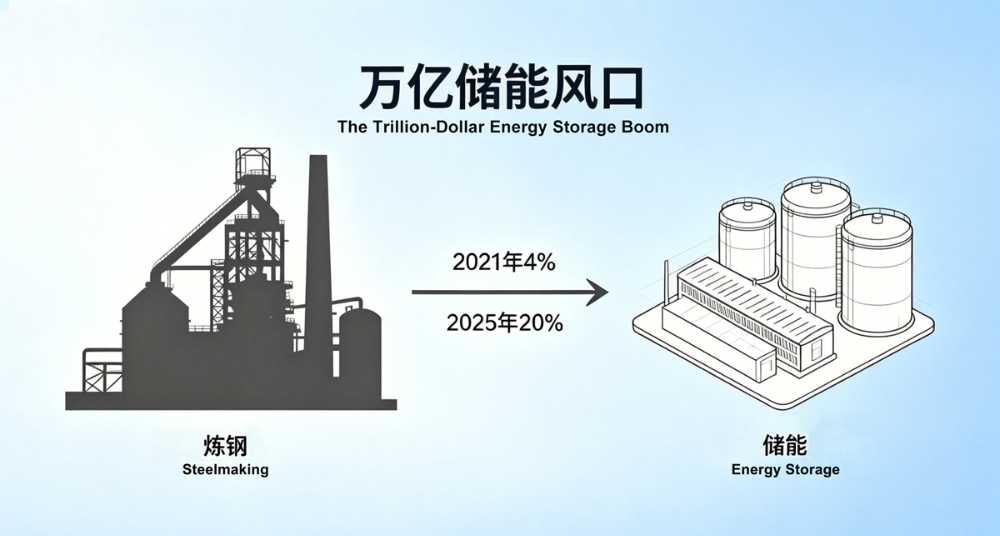

In recent years, China’s share of vanadium used in energy storage has surged from 4% in 2021 to an estimated 20% in 2025, while its share in steelmaking has dropped from 87.9% to 70.9%. Vanadium demand is shifting from a traditional metallurgical by-product to a core material in the emerging energy-storage sector.

This transition is driven by the rapid expansion of new energy storage under China’s dual-carbon goals. Among various technologies, vanadium redox flow batteries (VRFBs) have emerged as a leading solution for long-duration storage thanks to their inherent safety, 20-year lifespan, and zero capacity fade. As the “lifeblood” of VRFBs, vanadium electrolyte—accounting for over 40% of system cost—has become the key factor shaping industry economics and scale, creating unprecedented opportunities for resource owners and companies seeking new growth.

Surging Demand: A Trillion-Level Energy Storage Market and Rising Need for Vanadium Electrolyte

1. Rapid Market Expansion

The global vanadium electrolyte market is projected to grow from USD 2.28 billion in 2025 to USD 2.75 billion in 2026, reaching USD 15.24 billion by 2035—an impressive CAGR of 20.95%. This surge is driven by three key factors:

l Long-duration storage becomes essential:

For grid peak-shaving, renewable integration, and backup power, storage systems of 4+ hours are becoming standard. With inherent safety, 20+ year lifespan, and over 16,000 cycles, VRFBs are emerging as the optimal solution.

l Strong policy momentum:

China has included flow batteries in its key national demonstration roadmap. In January 2026, a new policy on capacity pricing reinforced the principle that “duration determines value,” directly favoring long-duration technologies like VRFBs.

l Resource security:

China holds 43% of global vanadium reserves, giving it a strong strategic advantage. Vanadium electrolyte thus becomes a critical, resource-secure alternative to lithium-based systems that depend heavily on overseas supply.

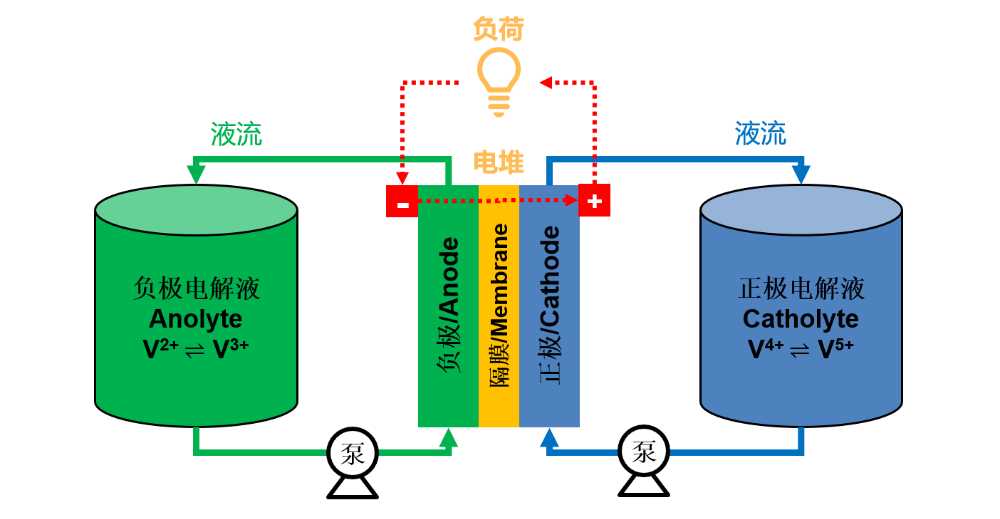

2. Vanadium Electrolyte: The “Blood” of VRFBs

Vanadium electrolyte consists of vanadium ions in different oxidation states dissolved in an acidic solution. Energy is stored and released through their redox reactions—meaning all energy in a VRFB is stored in the electrolyte. Its volume determines capacity, and its quality dictates system lifetime and efficiency. As the largest cost component, electrolyte is both the core material and the primary lever for cost reduction across the vanadium battery value chain.

Current Landscape: Accelerating Industrial Maturity and a Growing Capacity Gap

1. Supply Falling Short of Surging Demand

As of May 2026, China has over 600,000 m³/year of commissioned electrolyte capacity, yet a significant short-term supply gap remains.

Demand for vanadium pentoxide (V₂O₅) in energy storage is expected to rise from 32,000 tons to 60,000 tons in 2026. Electrolyte tenders exceed 6.5 GWh, corresponding to hundreds of thousands of cubic meters, far beyond stable domestic supply.

Most vanadium producers still focus on low–value-added products such as slag and V₂O₅, missing the rapid growth and higher margins of the electrolyte segment.

2. Global Market Growth with High Certainty

Worldwide demand growth for vanadium electrolyte is highly predictable.

According to QYResearch, the global market is valued at USD 904 million in 2025 and is expected to reach USD 2.16 billion by 2032, with a 13.4% CAGR.

China’s domestic CAGR is even stronger at 17.3% over the same period. Both growth rates indicate a high-prosperity track, with Chinese manufacturers set to maintain their leadership in global large-scale production.

3. Rapid Evolution of Technical Routes

Vanadium electrolyte production is dominated by two pathways:

Long-route process (mainstream):

Uses high-purity V₂O₅ and includes dissolution, reduction, and electrolysis.

It is the most mature, stable, and scalable process with wide process windows, strong controllability, and consistent product quality—ensuring purity, concentration, and valence stability suitable for long-life VRFB operation.

Short-route process (emerging):

Starts directly from vanadium-bearing leach solutions or industrial-grade raw materials, eliminating the need for high-purity V₂O₅. It shortens production steps, reduces material transfers, and lowers costs.

However, it still faces challenges such as lower maturity, insufficient impurity-removal precision, weaker stability, and incomplete supply-chain and standards, which limit large-scale adoption.

While the short-route offers greater cost-reduction potential, the long-route’s proven reliability and low trial-and-error cost remain significant advantages.

Future Trends: Performance Upgrades + Business Innovation Driving Long-Term Value

Performance optimization and business-model innovation will jointly accelerate industry maturation.

1. Performance Enhancements

R&D is increasingly focused on high-temperature stability, high-concentration electrolytes (for higher energy density), and wide-temperature-range formulations for harsh environments.

Among these, improving electrolyte stability under high-temperature conditions has become the most urgent priority. It directly increases utilization, reduces cost, enhances energy efficiency, and lowers operating consumption—key indicators for broader market acceptance of VRFB technologies.

2. Growing Industrial Maturity

VRFBs have entered the center of national policy attention, with multiple standards officially implemented from 2026 onward. The ecosystem is quickly shifting from rapid, unstructured expansion to a more regulated and standardized development path.

3. Business Model Innovation

Electrolyte leasing models—already adopted in several large-scale projects—can reduce upfront investment by 30–50%, significantly easing capital pressure for project owners.

Conclusion: The Moment Has Arrived

From surging demand and maturing technologies to supportive policies and a strengthening supply chain, the vanadium electrolyte industry is moving from demonstration to full commercial deployment. For mining companies with access to vanadium resources, this is not only a chance to extend the value chain and enhance product value, but also a strategic entry point into a trillion-RMB energy-storage market.

ZH Energy’s electrolyte production lines adopt a fully sealed design with a compact structure, easy transportation, and efficient installation—ensuring rapid commissioning and stable mass production for customers. To date, the company has delivered multiple electrolyte production lines in China and overseas. With proven technical reliability and fast delivery and service capabilities, it continues to provide stable support to global clients and has earned strong recognition in international markets.